Insurance Premium Calculator: Your Complete Guide to Estimating Coverage Costs

An insurance premium calculator is the easiest way to estimate how much your coverage will actually cost. Whether you’re searching for how much is insurance for your first home, comparing plans on a health insurance marketplace, or trying to figure out the right coverage for your growing family, one question keeps coming up: what will it actually cost? That’s exactly where an insurance cost calculator or premium estimator helps you make smarter decisions.

An insurance calculator or insurance estimator takes the guesswork out of coverage shopping. Instead of wading through policy documents or waiting on a broker, you can model dozens of scenarios in minutes, adjusting coverage amounts, deductibles, and term lengths until the numbers make sense for your budget and goals.

In this guide, we’ll break down every major type of premium calculator, explain the factors that drive your rates, and show you exactly how to build a free, interactive insurance premium calculator on Outgrow; no coding required.

What Is an Insurance Premium Calculator?

Table of Contents

An insurance premium calculator is an interactive tool, typically available online, that estimates how much you’ll pay periodically (monthly, quarterly, or annually) for an insurance policy. It combines your personal data with actuarial tables, coverage rules, and current market rates to produce a meaningful cost estimate before you commit to any plan.

At its core, every insurance estimator asks you a handful of fundamental questions: Who are you? What are you insuring? How much coverage do you need? And for how long? The answers feed into a formula that outputs a projected premium, often broken out by carrier, coverage tier, or deductible level.

Quick Fact

The word “premium” comes from the Latin praemium, meaning reward or prize. In insurance, it’s the price you pay to transfer financial risk to the insurer, and a good premium calculator for life insurance (or any other coverage type) helps you find the sweet spot between cost and protection.

Calculators exist for virtually every product in the insurance marketplace: life, health, home, auto, renters, disability, and long-term care. Each uses a different set of inputs, but the logic is the same, quantify your risk profile, match it to coverage options, and surface a price range.

Why You Need One Before Buying Coverage

- 40% of Americans are underinsured on life coverage

- 3x more accurate than agent ballpark quotes

- 15 min average time to run a full insurance estimate

- $600+ average annual savings from comparison shopping

Shopping without an insurance estimator is like buying a car without knowing its price. You might end up with great coverage, or you might overpay by hundreds of dollars each year. Here’s why running the numbers first is non-negotiable:

- Budget clarity: You’ll know exactly how a policy fits into your monthly cash flow before signing anything.

- Apples-to-apples comparisons: A good insurance calculator standardizes variables so you’re comparing equivalent coverage, not just price tags.

- Negotiation leverage: Walk into any broker meeting with a data-backed estimate and you’ll be far harder to upsell.

- Awareness of coverage gaps: Calculators reveal how much protection your family actually needs, not just what a basic plan offers.

- Healthcare marketplace navigation: On the healthcare marketplace, subsidies change dramatically with income, an insurance calculator helps you model different scenarios before you enroll.

“The best time to understand your insurance costs is before you need the coverage, not after you’ve already paid the premiums for years.”

Types of Insurance Premium Calculators

The insurance marketplace is vast, and each product category has its own dedicated calculator. Let’s walk through the most common types, what they measure, and who should use them.

Life Insurance Premium Calculator

A life insurance premium calculator estimates the cost of a policy that pays a lump sum (the death benefit) to your beneficiaries when you pass away. Inputs typically include your age, gender, health status, coverage amount, and policy type. The result is a monthly or annual premium for life insurance calculator output that helps you set a realistic budget for protecting your family’s financial future.

Term Life Insurance Premium Calculator

Term life is the most popular and affordable type of life coverage. A term life insurance premium calculator (also called a term insurance cost estimator or term policy pricing tool) estimates the cost for a fixed period (10, 20, or 30 years). Because term policies expire without payout if you outlive them, premiums are usually much lower than permanent coverage, making this life insurance premium estimator one of the most common choices for young families.

Whole Life Insurance Premium Calculator

A whole life insurance premium calculator accounts for permanent coverage that never expires and builds cash value over time. Premiums are higher than term, but a good premium life insurance calculator will show you the long-term value of the cash-value component alongside your ongoing cost obligation.

Single Premium Life Insurance Calculator

A single premium life insurance calculator (or one-time premium estimator) is used for policies funded with one large upfront payment instead of recurring premiums. It helps determine the minimum lump sum needed for a chosen death benefit. The related single premium whole life insurance calculator (or whole life lump-sum estimator) also factors in the guaranteed cash value growth of a whole life policy.

Return of Premium Life Insurance Calculator

A return of premium life insurance calculator models a unique hybrid: term coverage where premiums are refunded if you outlive the policy term. Because you’re paying for built-in return protection, premiums are higher, this calculator helps you evaluate whether the refund rider is worth the extra cost.

Health Insurance Premium Calculator

A health insurance premium calculator estimates monthly costs for medical coverage based on your age, household size, income, location, and plan tier (Bronze, Silver, Gold, Platinum). It’s an essential first step before exploring your options on the health insurance marketplace, since your income relative to the Federal Poverty Level directly determines your subsidy eligibility.

Home Insurance Premium Calculator

A home insurance premium calculator projects the annual cost of homeowner’s or renter’s coverage based on property value, location, construction type, credit score, and claim history. If you’re asking how much is insurance for a new property, this is the tool to start with. Many lenders require a home insurance estimate as part of the mortgage preapproval process, so running this calculator early can help keep your loan timeline on track.

Long Term Care Insurance Premium Calculator

A long term care insurance premium calculator projects the cost of coverage for extended care needs, nursing homes, in-home assistance, adult day programs, that health insurance typically doesn’t cover. Because premiums escalate sharply with age, this calculator is most valuable when used in your 40s and 50s, well before care is needed.

Key Factors That Affect Your Premium

No matter which insurance estimator you use, the same core variables drive your rate. Understanding these factors helps you interpret calculator outputs, and gives you actionable levers to pull if you want to lower your costs.

Age

This is the single biggest driver for a life insurance calculator premium output. The older you are when you apply, the higher the statistical likelihood of a claim, so insurers charge more. Every year you wait to buy term or whole life coverage increases your rate, sometimes significantly.

Health and Medical History

Insurers evaluate current health conditions, BMI, smoking status, family medical history, and recent prescriptions. A term life insurance premium calculator will show dramatically different results for a non-smoker versus a tobacco user, often a 200–300% rate difference for the same coverage amount.

Coverage Amount and Term Length

Larger death benefits and longer policy terms both increase premiums. A term insurance premium calculator lets you model different combinations, perhaps $500,000 for 20 years versus $1,000,000 for 10 years, to find the sweet spot for your family’s needs and budget.

Policy Type

Term, whole, universal, and variable life policies all have different pricing structures. A whole life cost estimator will return a higher estimate than a comparable term life estimator because whole policies are permanent and build cash value.

Income and Subsidy Eligibility

For the health insurance marketplace, your household income relative to the Federal Poverty Level determines whether you qualify for premium tax credits. A health insurance cost estimator that includes subsidies can show a net monthly cost much lower than the listed price.

Location

State regulations, local healthcare costs, and regional disaster risk all affect premiums. A home insurance cost estimator in a flood-prone or wildfire-risk area will return much higher estimates than a property coverage tool in a low-risk ZIP code with the same home value.

Credit Score

In most states, insurers use credit-based insurance scores to price home and auto policies. Improving your credit before using a home insurance cost estimator or coverage pricing tool can meaningfully shift your estimate.

Comparing Calculator Types: A Quick Reference

| Calculator Type | Best For | Key Inputs | Typical Monthly Range |

| Term Life Insurance Premium Calculator | Families, young professionals | Age, health, term, coverage amount | $15 – $80 |

| Whole Life Insurance Premium Calculator | Estate planners, high earners | Age, health, face value, riders | $200 – $1,000+ |

| Single Premium Life Insurance Calculator | Retirees, lump-sum investors | Age, health, desired death benefit | One-time $25k – $500k+ |

| Return of Premium Life Insurance Calculator | Risk-averse buyers | Same as term + refund rider cost | $40 – $200 |

| Health Insurance Premium Calculator | Self-employed, marketplace shoppers | Income, age, family size, ZIP | $200 – $800 (pre-subsidy) |

| Home Insurance Premium Calculator | Homeowners, buyers | Home value, location, credit | $80 – $250 |

| Long Term Care Insurance Premium Calculator | Adults 45–65 planning ahead | Age, health, benefit period, inflation | $150 – $400 |

How to Build an Insurance Premium Calculator with Outgrow

If you run a financial services site, an insurance agency, or a personal finance blog, offering an interactive insurance cost estimator can boost engagement, generate qualified leads, and build trust with your audience, all without writing a single line of code. Outgrow’s premade Insurance Cost Estimator template provides a conversion-optimized foundation you can customize in minutes.

Here’s exactly how to build your own branded insurance premium calculator using Outgrow’s no-code platform:

Sign up and select the calculator template

Create a free Outgrow account and navigate to the Templates library. Search “insurance” and open the Insurance Premium Calculator premade template. This gives you a fully functional, conversion-tested structure to build on.

Add your core qualifying questions

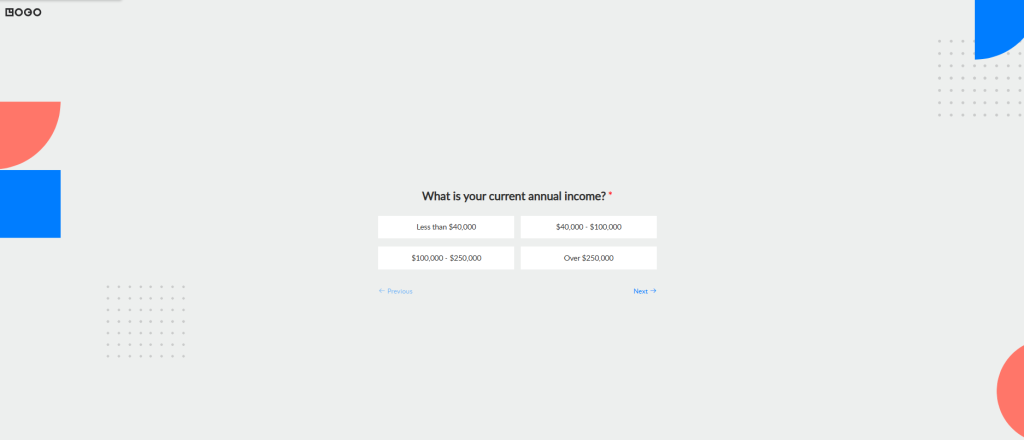

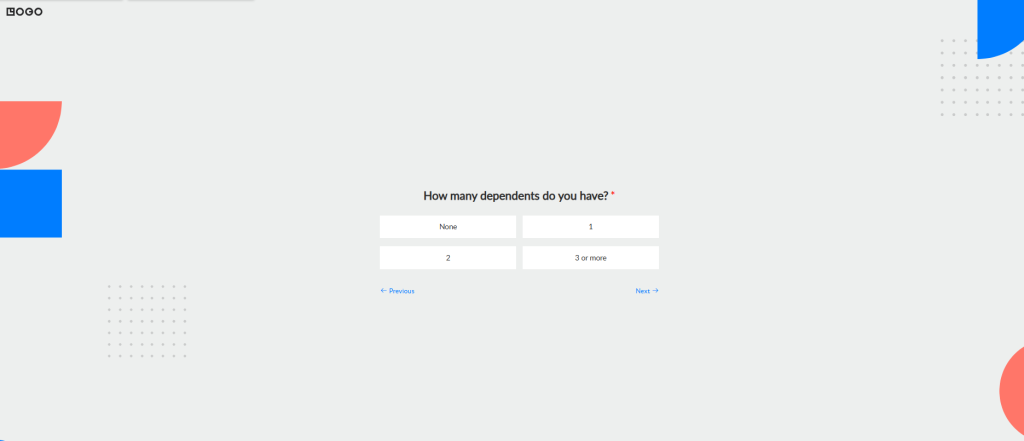

The Insurance Premium Calculator template supports fully customizable question flows. Use Outgrow’s drag-and-drop builder to add, reorder, or rephrase questions to match your audience. The eight questions below form the backbone of an effective life insurance premium estimation flow, add them in order for the clearest user journey.

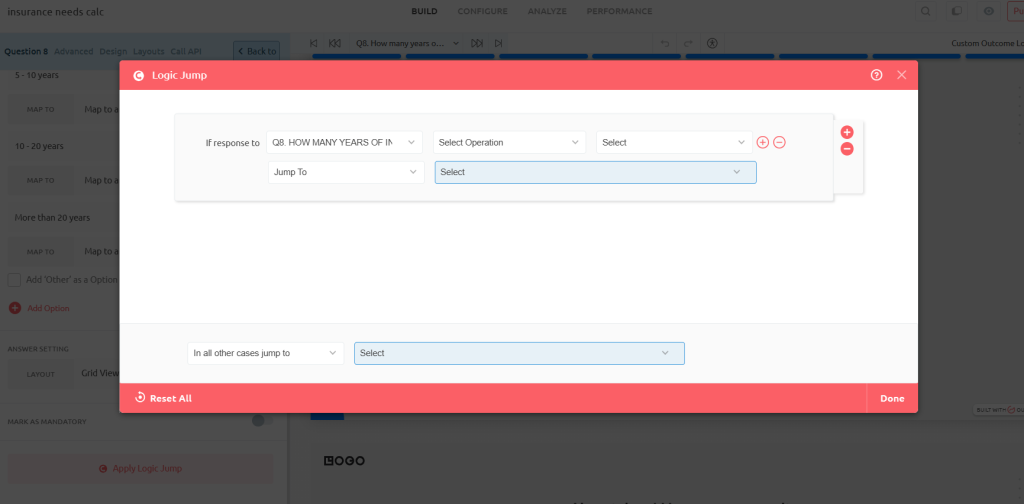

Configure logic, scoring, and outcome formulas

Outgrow’s formula builder lets you assign weights to each answer and calculate a personalized premium range. Use conditional logic to branch paths, for instance, showing different follow-up questions for users who indicate outstanding debt versus those who are debt-free.

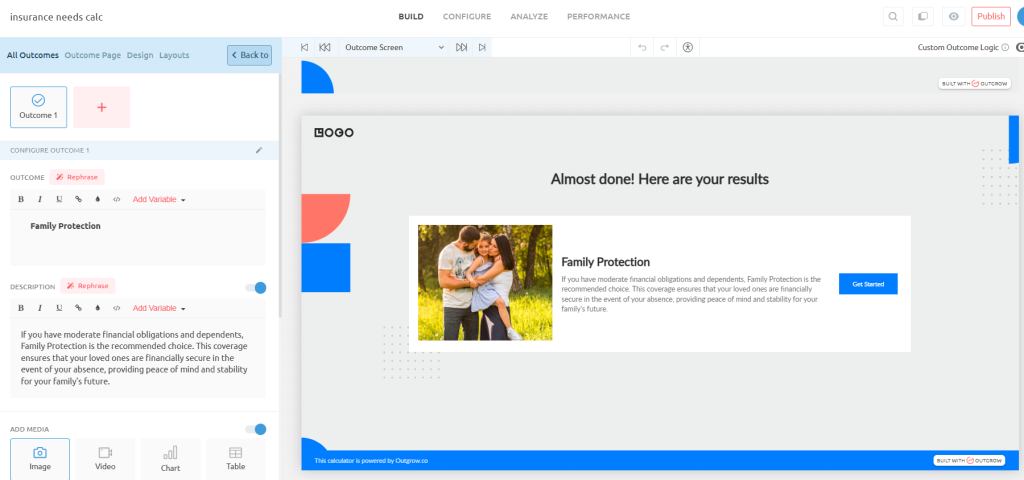

Design your results page

The results screen is your most valuable real estate. Display the estimated premium range clearly, add educational context about term life and whole life cost estimates, and include a strong call to action (speak to an advisor, request a quote, or download a report).

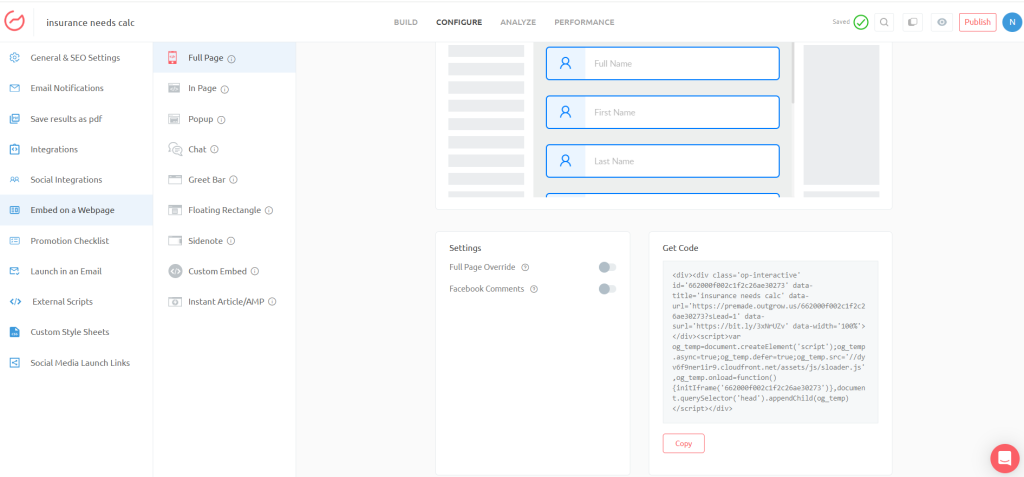

Brand it, embed it, and connect your CRM

Apply your brand colors, logo, and fonts. Then publish your insurance estimator as an embedded widget, a pop-up, or a standalone page. Connect Outgrow’s native integrations (HubSpot, Salesforce, Mailchimp, and more) to automatically route leads to your pipeline the moment someone completes their estimate.

The 8 Questions to Include in Your Calculator

Add these questions to your Calculator template for a comprehensive, data-driven estimate:

- What is your current annual income?

- How many dependents do you have?

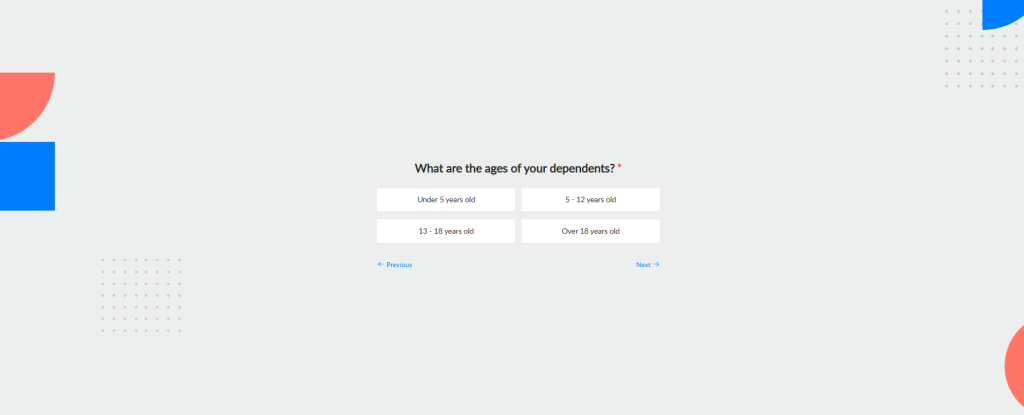

- What are the ages of your dependents?

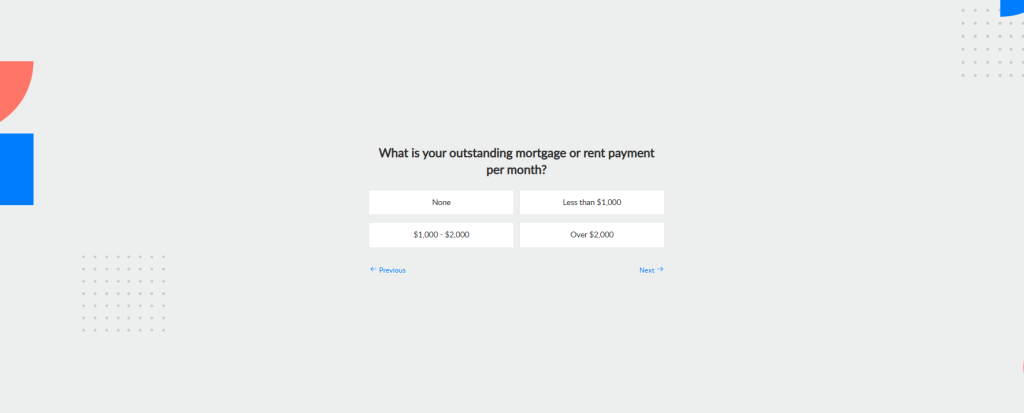

- What is your outstanding mortgage or rent payment per month?

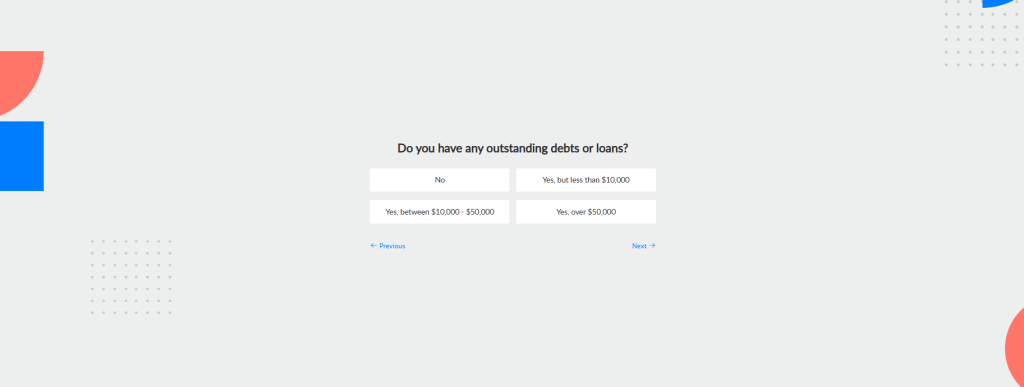

- Do you have any outstanding debts or loans?

- How much do you have saved in emergency funds?

- What are your future financial goals or obligations?

- How many years of income replacement do you want to provide for your family?

These questions collectively cover every critical variable in a life insurance premium calculator: income replacement need, dependency load, debt obligations, existing financial cushion, and desired coverage duration. Together they produce a tailored estimate that’s far more meaningful than a generic insurance estimator based on age alone.

Pro Tips for Getting the Most Accurate Estimate

A life insurance cost estimator, or any insurance pricing tool for that matter, is only as good as the data you put into it. Follow these best practices to make your estimates as reliable as possible:

Use your actual income, not a round number

Most insurance cost estimators use income to determine coverage adequacy. Whether you’re running a life insurance cost estimate or navigating the health insurance marketplace, inputting your precise adjusted gross income (from your last tax return) produces a far more accurate result than a rough approximation.

Include all dependents, even adult ones

A term life policy estimator typically focuses on minor children, but many families also support aging parents, adult children in school, or partners with limited income. Including all financial dependents gives you a more honest picture of your coverage needs.

Factor in debt obligations

Your insurance estimate outputs should account for mortgage balances, car loans, student debt, and credit lines. These obligations don’t disappear when you do, and a thorough life coverage estimator should incorporate them into its recommendation.

Re-run the calculator after major life events

Marriage, divorce, the birth of a child, a home purchase, or a significant income change, all of these are triggers to revisit your insurance estimator. What was adequate coverage five years ago may leave your family dangerously exposed today.

Compare term and whole life side by side

Use both a term life cost estimator (or term policy pricing tool) and a whole life cost estimator (or whole life pricing tool) together to compare costs. For most families with simple protection needs, term coverage offers more value per rupee, but a life insurance comparison tool lets you decide using real numbers instead of assumptions. For policyholders who already own permanent coverage they no longer need, understanding the life settlement market can also help them evaluate options beyond keeping, surrendering, or lapsing the policy.

Model the return-of-premium upgrade

If you’re considering a rider that refunds your premiums if you outlive the policy, run a dedicated return-of-premium estimator to see the exact cost difference. The upgrade typically adds 20–50% to your base premium, a real number to weigh against the psychological value of the refund guarantee.

Use marketplace subsidies for healthcare

If you’re using a health insurance cost estimator for marketplace coverage, always input your household income to check subsidy eligibility. In the healthcare marketplace, many households qualify for substantial premium tax credits that make Silver and Gold plans far more affordable than their listed prices.

Final Thoughts

Whether you’re comparing plans on the health insurance marketplace, modeling a term life insurance premium calculator for your family, or finally getting serious about the coverage you’ve been putting off, the right insurance premium calculator is the most powerful first step you can take.

The data is clear: people who use an insurance estimator before buying coverage get better rates, more appropriate coverage amounts, and spend less time second-guessing their decisions. And for financial services businesses, offering an interactive insurance calculator isn’t just a helpful user tool, it’s one of the highest-converting lead generation assets available.

“The right insurance premium calculator doesn’t just tell you what you’ll pay, it helps you understand what you actually need.”

From the premium calculator for life insurance to the long term care insurance premium calculator, each tool in this category serves the same ultimate purpose: giving you confidence that your financial safety net is real, adequately sized, and priced fairly. Use them, compare them, and revisit them as your life changes.

And if you want to offer this value to your own audience, the Insurance Premium Calculator on Outgrow is the fastest path from idea to live, lead-generating tool, with the eight essential questions already mapped out above to get you started.

Frequently Asked Questions: Insurance Premium Calculator:

A general life insurance cost estimator models multiple policy types, including term, whole, universal, and variable. A term life policy estimator is designed for temporary coverage with a fixed end date.

A quality insurance estimator is typically accurate within 10–20% of your actual approved rate, pending underwriting. The main source of variance is health classification, most calculators assume “standard” health, while your actual rate may be better (preferred, preferred plus) or worse depending on your medical history.

Yes. Platforms like Outgrow provide premade insurance cost estimator templates that require no technical knowledge. You configure your questions (like the eight listed in our Outgrow tutorial above), set your formula logic, brand the experience, and embed it on your website using a visual drag-and-drop interface.

Ankit Upadhyay is a Digital Marketing and SEO Specialist at Outgrow. With a passion for driving growth through strategic content and technical SEO expertise, Ankit Upadhyay helps brands enhance their online visibility and connect with the right audience. When not optimizing websites or crafting marketing strategies, Ankit Upadhyay loves visiting new places and exploring nature.