Debt-to-Income Ratio Calculator: The Number Lenders Look at Before Anything Else

Table of Contents

My friend applied for a mortgage last spring. Good job, decent savings, zero missed payments in years. Got declined. The loan officer told her the issue wasn’t her credit score. It was her DTI. She’d never heard the term before that conversation.

That’s more common than most people realize. Lenders don’t just look at what you earn. They look at what’s already spoken for. And if too much of your paycheck is committed to existing debts, a new loan gets much harder to get, no matter how responsible you’ve been.

That’s the whole point of a Debt-to-Income Ratio Calculator. You put in your numbers, it tells you what a lender will see, and you decide what to do about it before anyone else is involved. No surprises in the closing office. No awkward calls from underwriting.

So What Actually Is DTI?

Your debt-to-income ratio is just a percentage. Specifically, it’s the chunk of your gross monthly income (before taxes, before anything gets taken out) that goes toward paying debts you already owe.

The calculation itself isn’t complicated:

DTI = (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100

Walk through a real example. You earn $6,500 a month before taxes. Your rent is $1,300. Your car payment is $420. The student loan minimum is $180. The credit card minimum is $75. That’s $1,975 per month in debt obligations. Divide by $6,500, multiply by 100, and you land at 30.4%.

Lenders read that number roughly like this:

- Under 36%: Most lenders are comfortable here. You’re seen as a manageable risk.

- 36% to 43%: Still qualifiable for most loans, but expect more questions and possibly worse rates.

- 44% to 49%: Getting into yellow-flag territory. A fair number of lenders won’t touch this range.

- 50% and above: Conventional products become very difficult to access at this level.

What a Debt-to-Income Ratio Calculator does that simple math on a napkin doesn’t is show you the breakdown. Which payment is pulling your percentage up most? What happens if you pay off the car early? What if you pick up a freelance client and add $800/month to your income? The calculator lets you model all of it before you’re sitting across from an underwriter.

What Goes In and What Gets Left Out

People consistently overestimate their DTI because they’re counting things that don’t belong in the formula.

Debt payments that count:

- Monthly mortgage or rent payment

- Car loan payments

- Student loan minimums

- Minimum credit card payments

- Personal loan payments

- Any court-ordered payments like child support or alimony

Things that don’t count, even if they feel significant:

- Electricity, water, gas bills

- Groceries and household goods

- Car insurance or health insurance premiums

- Phone bill

- Gym memberships, streaming services, subscriptions

- Out-of-pocket medical costs

The distinction matters more than it seems. Someone might be spending $4,800 a month total but only have $1,600 in actual debt obligations. Those are two wildly different numbers, and a Debt-to-Income Ratio Calculator works off the second one.

One more thing worth understanding: there are actually two DTI numbers that come up in mortgage situations. Front-end DTI is housing costs only, and lenders typically want that under 28%. Back-end DTI is everything combined, and most want that under 43%, though some programs go higher. A good calculator surfaces both, so you’re not surprised when a mortgage broker brings them up.

Why Your Income Number Alone Doesn’t Save You

This misconception comes up constantly. People assume that once they’re earning a certain amount, loan approvals follow automatically. Lenders don’t work that way.

Take two applicants:

First person earns $11,000 a month. Has a mortgage, two car payments, and student loans totaling $5,280 per month in obligations. DTI lands at 48%.

Second person earns $4,800 a month. Has rent and one small car payment totaling $1,390. DTI comes in at 29%.

The second applicant gets better rates and less friction, almost without exception. Their income is less than half as much. But the ratio is what lenders price off of, not the raw dollar amount coming in.

Running a Debt-to-Income Ratio Calculator before you apply reframes the whole question. You stop asking “do I earn enough?” and start asking “is my ratio where it needs to be?” Those are different problems with different solutions, and knowing which one you’re actually dealing with changes what you do next.

DTI gets checked in more places than people realize, too:

- Auto dealers and their financing partners factor it in even when the conversation stays focused on monthly payment amounts.

- Personal loan lenders lean heavily on DTI because there’s no property or asset backing the loan.

- Small business owners often find their personal DTI gets scrutinized alongside business financials during loan applications.

- Refinancing triggers a full DTI review even when you’re not borrowing anything new.

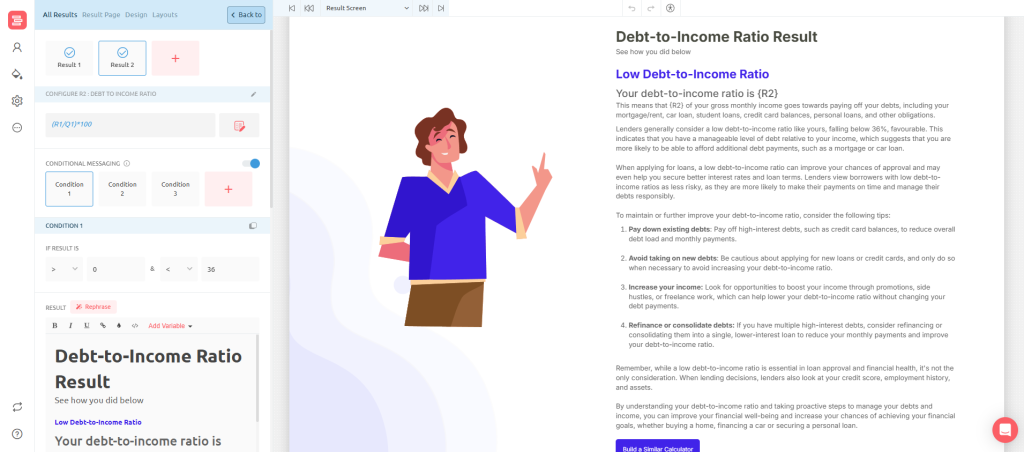

How Outgrow’s Interactive Content Helps Your Decision

Most financial calculators online are a box, a button, and a number. You put your information in, you get a percentage back, and then you’re on your own trying to figure out what that percentage actually means for your situation.

Outgrow takes a different approach to the Debt-to-Income Ratio Calculator experience. The math is still there, but the output goes further.

Context gets built into the result. A 46% DTI means one thing if you’re applying for a conventional 30-year mortgage and something completely different if you’re looking at an FHA loan or a VA product. Outgrow’s conditional logic lets the result screen adapt to what the user said they were trying to do, not just spit back a decontextualized percentage.

The next action becomes obvious. If someone’s sitting at 48% and needs to get under 43%, a well-built calculator tells them they need to cut roughly $X from their monthly obligations, and can flag which debt category would get them there fastest. That’s a useful output. A raw percentage with no interpretation is not.

High-intent leads get captured. Anyone who just ran a DTI calculation is actively thinking about borrowing money. For mortgage brokers, financial advisors, or anyone in lending, that’s an extraordinarily qualified moment to collect contact information. An Outgrow-built Debt-to-Income Ratio Calculator can gate the full result behind a simple lead form, so the tool is generating contacts, not just traffic.

The calculator belongs to your site. Your brand, your domain, your copy. Not a widget pointing back to someone else’s platform.

Try Outgrow’s Ready-to-Use Debt-to-Income Ratio Calculator

There’s already a pre-built Debt-to-Income Ratio Calculator template inside Outgrow. You don’t have to start from a blank page.

The template comes with:

- Income input fields covering salary, self-employment, rental, and other sources

- Separate fields for each major debt category

- A visual output showing where the result falls against standard lender benchmarks

- Personalized result text that changes based on which DTI range someone lands in

- An optional lead capture step before the result is revealed

Head to Outgrow, open a free account, pull up the DTI template, and you can have a live version on your website before the day is out. No developer required, no code to write.

For anyone running a site in financial services, mortgage, real estate, or personal finance content, a working Debt-to-Income Ratio Calculator outperforms almost every other tool for capturing visitors who are actually close to a financial decision. Static blog posts get read and forgotten. A calculator gets used, bookmarked, and shared.

Building Your Own Debt-to-Income Ratio Calculator with Outgrow

If the pre-built template doesn’t quite fit what you need, building a custom version takes one focused afternoon. Here’s how it actually goes:

Step 1: Pick the Calculator content type in Outgrow’s builder.

This sets up the architecture for formula-driven outputs. Takes about thirty seconds.

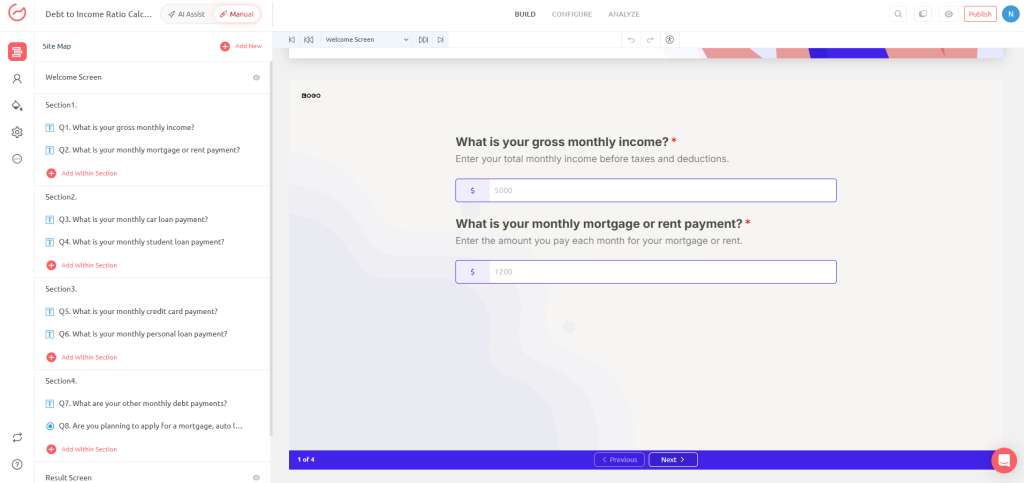

Step 2: Add your input fields.

Gross monthly income goes first. Then individual fields for each debt type: mortgage or rent, car payments, student loans, credit card minimums, personal loans, anything else your specific audience carries. Label them the way your users would think about them, not how a bank form would phrase it.

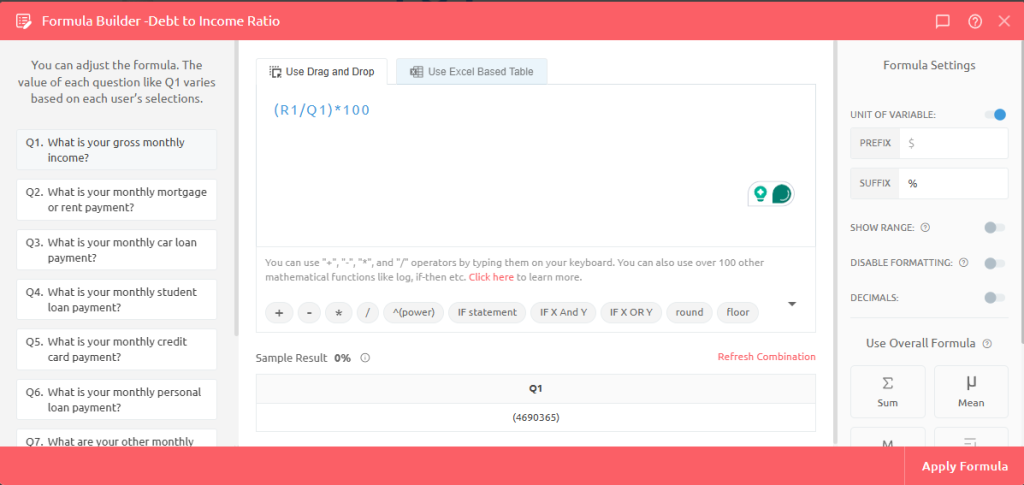

Step 3: Write the formula.

Inside Outgrow’s formula builder: sum of all debt fields, divided by the income field, multiplied by 100. No coding syntax to learn. It reads like regular math.

Step 4: Build result screens for each range.

Four tends to work well: strong position, acceptable, borderline, needs attention. Each screen gets its own message, its own explanation of what that result means, and its own call to action. The person at 29% and the person at 51% should be reading completely different things.

Step 5: Apply your branding.

Logo, brand colors, font choices. This part usually takes under fifteen minutes and makes the difference between something users trust and something that looks like a generic bank widget.

Step 6: Publish and embed.

Copy the embed code Outgrow generates, paste it into your site, and the Debt-to-Income Ratio Calculator is live. Ongoing maintenance is minimal.

Who Actually Gets Value From This

The individual borrower trying to prep for a loan application is the obvious user. But the professional applications are where things get interesting.

First-time homebuyers almost never know their DTI when they start looking at homes. They know their salary, and they know what they can afford in monthly payments, but the ratio itself is a blind spot. A calculator fixes that before they fall in love with a house they can’t qualify for.

Self-employed people have a harder time with DTI calculations because their income isn’t a clean monthly number. A calculator that can handle variable income, multiple income streams, and seasonal fluctuations helps them figure out when their numbers are strongest and time applications accordingly.

People thinking about debt consolidation need to know whether rolling several debts into one personal loan will actually change their DTI or just rearrange it. The answer isn’t always obvious, and the Debt-to-Income Ratio Calculator makes it visible immediately.

Loan officers and mortgage brokers can use a branded calculator as a soft pre-qualification step. Clients who’ve already worked through their DTI before the first call arrive with more realistic expectations and far fewer surprises in the underwriting process.

Financial educators and coaches get a tool that creates immediate, tangible value for their audience before any money changes hands or any session gets booked.

Actually Moving the Number

You ran the Debt-to-Income Ratio Calculator, and the output wasn’t what you wanted. Here’s what genuinely works to change it:

Eliminate a payment rather than reduce a balance.

Paying a $380 car loan down to zero does more for your DTI than paying $380 off each of five different credit card balances. Lenders count the number of active payment obligations. Getting rid of one entirely has an outsized effect compared to reducing several partially.

Don’t open anything new before applying.

It seems obvious, but people still do it. The store card you opened to get a 15% discount, the phone on a 24-month installment plan, the furniture you put on financing. Every new monthly obligation increases your DTI at the exact moment you need it to stay flat or drop.

Work both sides of the ratio.

Adding income lowers DTI just as effectively as cutting debt, sometimes faster. A consistent freelance client, a part-time role, rental income from a spare room. The formula doesn’t care how you improve the ratio, only that you do.

Audit what’s being reported as active.

Paid-off accounts that still show as open with a balance, debts discharged in settlements that lenders still count, old collections that shouldn’t be there. These inflate what lenders calculate as your monthly obligations. Worth checking well before you apply, not the week of.

Rerun the Debt-to-Income Ratio Calculator after each adjustment. Concrete feedback on what’s working beats motivation speeches every time.

Walk In Knowing the Number

There’s a real difference between borrowers who get good terms and borrowers who don’t, and it’s often not income. It’s preparation. The ones who come out ahead walked in knowing exactly what the lender was going to find. They’d already run the Debt-to-Income Ratio Calculator, identified the weak spots, and addressed what they could before the conversation started.

If you’re advising people making these decisions, or if your audience is thinking about loans and credit, a working calculator on your site is one of the most direct ways to demonstrate you actually understand their situation. Not a blog post explaining DTI in theory. A tool that processes their actual numbers and tells them where they stand.

Sign up for Outgrow’s 7-day free trial and get your Debt-to-Income Ratio Calculator live today. The people in your audience working through these numbers right now deserve a real answer, not a generic explanation.

Frequently Asked Questions

Most lenders get comfortable below 36%, with housing costs specifically under 28% of gross monthly income. Between 36% and 43%, you can still qualify for plenty of products, but expect higher scrutiny. Above 50%, and most standard options are off the table.

Not even slightly. The calculator is just arithmetic; it has no connection to any credit bureau and generates no inquiry. Your score only moves when a lender formally pulls your credit file during an actual loan application.

Utilities, groceries, insurance premiums, phone bills, and subscriptions are all excluded. DTI only counts legally obligated recurring debt payments. If you could stop paying it tomorrow without defaulting on a signed agreement, it almost certainly doesn’t factor in.

Yes. Outgrow produces an embed code when you publish, and you paste it into any page on your site. It runs fully within your domain, carries your branding, and can be set up to collect contact information before showing the result.

Whenever anything meaningful changes- a debt gets paid off, income goes up or down, a new payment gets added. For anyone planning a loan application within the next six to twelve months, checking the Debt-to-Income Ratio Calculator every couple of months keeps you from getting blindsided.

Front-end covers housing costs only, and lenders want it under 28%. Back-end covers every debt obligation combined, which is what underwriters spend most of their time on. High back-end with a clean front-end usually means car loans or student debt are the problem, not your housing payment.

Sakshi is a digital marketing enthusiast passionate about connecting brands with audiences. With a background in content strategy and social media, she loves turning trends into actionable strategies. Outside of work, you’ll find her reading a book or hunting for the perfect cup of coffee.